The Student Loan Trap

Rodney Spangler first enrolled at the University of North Texas in 2001. There, he pursued a degree in what the school now calls “integrative studies,” focusing on history, philosophy, and criminal justice. Rodney also worked full time, and so attended UNT on and off until 2007.

For every semester of classes, Spangler took out student loans. When he left—without a degree—he estimates that he had about $30,000 in outstanding student debt.

“At first I always intended to repay them, but the first time I took a semester off, I started getting due notices/bills for them,” Spangler told The American Conservative by email. “[I s]tarted going back, but the ones that came due kept sending notices, like there was no ‘pause’ button.”

Overwhelmed by bills, Spangler simply stopped paying. Today, thanks to interest and delinquency penalties, he estimates his outstanding debt is about $60,000—double what it was. “I just don’t see how I can ever pay those off,” Spangler wrote, “short of winning the lottery.”

Of course, it’s possible to go on living with a five-figure debt hanging over your head, but it imposes more than its fair share of limitations. When Spangler tried to get a job in law enforcement, he met all the requirements, but was denied because of his credit history.

“I had some of the highest placement scores they had seen,” Spangler claims, “but my credit report had too many negative marks.” With one or two exceptions, all of those marks were from student loans.

The weight of the debt has not only hindered Spangler’s search for employment—it has also affected his family and romantic life. He has had to rely on his parents to cosign for loans. And, he says, he has been “a little reticent to pursue a serious relationship,” thanks in part to fear of being judged for his debt.

Spangler is not alone: he’s one of the 44 million Americans who holds student debt, 30 percent of the population who have attended college. Together, they owe about $1.5 trillion, a bigger burden than credit cards, auto loans, or any other non-mortgage debt.

That there is a student debt crisis is not news. Media sites report on it frequently; academics attend to it with increasing trepidation. But in focusing on the scale of the problem, we sometimes forget to think about how all that debt affects people’s lives.

Specifically, the last 20 years of student debt accumulation—driven largely by federal policy—have radically shifted the life-courses of younger Americans, whether late Gen Xers like Spangler or Millennials. Millions of Americans now enter adulthood with a burden unfaced by their parents or grandparents, which in turn slows their family formation, alters labor market behavior, and represents a profound alteration to how they live out citizenship.

Americans, historically, had little schooling. In 1900, less than 10 percent went to or graduated from high school; by 1910, the median adult had completed only 8 years of schooling. Americans, since Tocqueville’s time at least, have believed that education was the nursemaid of citizenship. But only recently has that come to mean more than primary schooling.

The modern, post-war economy, however, precipitated a radical change in America’s educational composition. In 1962, just 19 percent had been to college; today, 61 percent have. The proportion actually graduating went from 9 to 35 percent in the same period. In short, over the past half century, higher education has gone from the exception to the norm.

Stretching back at least to the G.I. Bill, government has carried the lion’s share for this transition. In 1965, the government began to offer its credibility as a guarantor of private student loans under the Federal Family Education Loan Program. In the early 1990s, the Department of Education started issuing student loans itself, under the Federal Direct Loan Program.

The amount of debt held by the DOE rose steadily through the 1990s and early 2000s, then exploded during the Great Recession. Preston Cooper, an education research analyst at the American Enterprise Institute, told TAC that many Americans, forced out of the full-time workforce, opted to reskill—and took on lots of debt to do so. The feds funded that choice: as of 2015, 91 percent of all student loans were publicly held.

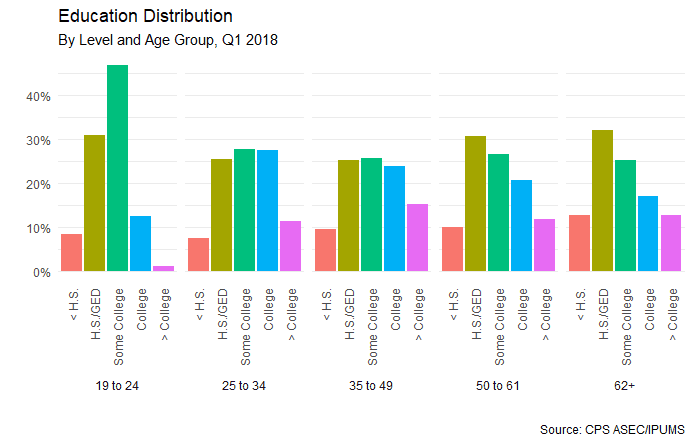

Publicly available data on federal student loans thus get us most of the way to a picture of the student debtor population. Those data show that as federal loans became readily available, millions of Americans took them on.

Clearly, some older Americans—especially ages 35 to 49—have debt, likely thanks to grad school and the Great Recession reskilling. But there is a pronounced disjuncture between even that group and America’s younger adults. Among those who have attended (although not necessarily graduated from) college, more than half are in debt.

We can look closer for an even starker picture. The mode 25- to 34-year-old debtor has between $20,000 and $40,000 of debt—the median annual salary for a recent college grad is about $50,000. Americans currently in and fresh out of college owe similarly high amounts.

Maybe student debt is not so bad. As David Leonhardt argued in a recent New York Times op-ed, it is in large part held by college-educated kids from the top income quartile, who can expect a substantial wage premium. Student debtors are likely to be well-off, and a college degree will make them more so.

Two issues complicate this argument, however. The first is what we might call the “Somes”: those who, like Spangler, have more than a high school degree but less than a college degree, i.e. only “some” college experience. Federal survey data show that “Somes” account for the second-highest proportion of all adults and the highest proportion of 25 to 34 year-olds.

Whereas debt-holding college grads usually do well, Somes don’t. Essentially all of the college wage premium accrues upon graduation, thanks to what economists call the “sheepskin effect”—the earnings boost comes with the diploma.

The obverse of this is that Somes end up looking more like their peers with a high-school degree than a college one—except, that is, for a lot of student debt. As Leonhardt notes, 40 percent of Some borrowers defaulted on their loans, compared to just 8 percent who graduated. For a significant part of the student-loan-debtor population, then, there is no college-degree cushion.

There’s a bigger problem: even among grads, student debt slows the set of life choices we commonly associate with adulthood. Even if most debtors eventually get their lives on track, debt has substantial effects on how long it takes them to do so.

Unsurprisingly, having debt shapes young Americans’ job market decisions. Researchers at the University of California, Berkeley found that grads with debt pick higher salary jobs, often over “public-interest” positions. They also found that bearing debt may affect students’ “academic decisions during college” in a way likely tied to their ultimate career trajectory. Young Americans may be more cautious about entering low-paying, high-social-significance roles—including politics, an area where older Americans are conspicuously over-represented.

Then there’s homeownership. Americans in their 20s have always been unlikely to buy, but Millennials may be delaying well into their 30s. The couple profiled in a recent Politico article on Millennials’ homebuying were 32 and 33, respectively; both cited their student debt as delaying their purchase. Analysis of British homeownership trends shows this is a common phenomenon, linking increased student debt levels to a “delay” in “first-time homeownership transition.”

All of this contributes to late family formation. Fewer young adults are married than ever and multiple analyses have found that student debt encourages cohabitation and reduces marriage among college-educated women (although, interestingly, not among men). That translates into less sex, and correspondingly fewer kids. A New York Times/Morning Consult poll found that 64 percent of young adults had fewer kids because of the cost of childcare (and, presumably, their ability to meet it); among those who claimed not to want kids, 13 percent explicitly cited their student debt as the reason.

All of this is fairly intuitive—if you have five figures of debt, paying it down will inevitably require trade-offs, which means delaying life. But it means that college debt directly slows young adults on the path their parents enjoyed—homes, marriage, children, etc.

That’s the big problem. Even bracketing the Somes, spiraling student debt has had a lasting impact on how hard young Americans have to work just to make it to the same place as previous generations. The new normal of debt necessarily alters the shape of American life.

Crushing debt and delayed lives are of course unpleasant individual experiences, but there is a deeper problem of political equity. In America, there is a strong connection between education and the ideal of citizenship—a republic requires an educated populace. This connection implicates more than just reading and writing—Eleanor Roosevelt contended that every discipline, from Latin to mathematics, informs good citizenship.

In a society where education is a prerequisite for civic participation, raising the floor of expected educational attainment, we thought, would make better citizens. This was, for example, the instinct which induced President Barack Obama to call on “every American to commit to at least one year or more of higher education or career training…. every American will need to get more than a high school diploma.”

But what is meant as inclusionary ends up exclusionary. The explosion of student debt, with its concurrent effects on debtors’ lives, means that many who go to college struggle along on the path to full, independent American life. Deviations from life course constrain young Americans in their ability to give back to their communities, to raise families, to buy homes, to teach responsible membership in society—in short, to be a citizen. The debt-financed education revolution risks retarding precisely the democratic goal it was meant to serve.

When we spoke, Rodney Spangler was 39, almost 40. He intends to go back to school next fall. He will still be heavily in debt, although perhaps finally getting a degree will help. Even so, he’ll have worked for decades for a position his parents could have reached with a high school education.

The proportion of the population that is college-exposed broke 50 percent in 2000 and has risen steadily since then. According to the Pew Research Center, the rising generation of “post-Millennials” are expected to be the most educated ever, with nearly 60 percent of those over 18 enrolled in college. If, as so many have argued, a new generation needs a renewed commitment to American citizenship, then they also need help surpassing the limitations stopping them from most fully living that commitment.

Charles Fain Lehman is a staff writer for the Washington Free Beacon. He writes about policy, covering crime, law, drugs, immigration, and social issues.