The Debtor’s Road to Peace and Prosperity

Cicero famously described infinite money as the sinews of war. The ability to mobilize greater wealth than ready cash provided gave countries tremendous advantage during the struggles of the early modern era. Britain’s capacity to leverage credit backed by profits from growing overseas trade facilitated its rise as a great power after 1688. As well as supporting its own military and naval forces, 18th-century Britain financed allies through wartime subsidies that bought political influence. Wealth backed diplomacy through the long rivalry with France that ended at Waterloo; it also provided influence during the long 19th-century peace that followed until 1914.

Paradoxically, however, borrowing can provide leverage of its own. Benjamin Franklin shrewdly observed that having someone do a favor for you gets him on your side more surely than doing one for him, as now he has a stake in your future. The same principle operates among states. Jennifer Siegel’s For Peace and Money presents as an example Russia from the start of extensive lending in the 1890s through a 1922 Russian default that devastated creditors. Far from costing the country its independence, she argues persuasively that the relationship strengthened Russia politically. France and Britain needed both to secure investments and keep Russia from aligning with Germany. Debt thus provided Russia with leverage more typically associated with wealth. Siegel, a prize-winning historian whose earlier work explored the geopolitical impact of Anglo-Russian rival in Central Asia, shows the complexities behind the truism that financial power sets the foundation for political strength.

Besides adding to historical scholarship on diplomacy surrounding World War I, Siegel’s lucid, well-informed analysis engages questions relevant to today’s concerns. Debt crises since the late 1970s have tested the influence of creditors over governments to which they lend. Since the notorious Russian defaults after World War I, wealthy governments have not been able to protect creditors by placing debtor countries into a form of receivership, supervising their internal finances as they did with Egypt and the Ottoman Empire during the 19th century. Finance ministries instead have brokered plans to reschedule payment, in order to ease the burden on debtors while shielding the own countries’ banks from the consequence of full default.

While negotiations often impose a haircut on creditors pushed to accept less than full payment, they also involve stipulations on debtor economies. The recent Greek bailout imposed a painful austerity that sparked popular resentment. Italy has faced similar pressure from its European Union partners to restructure public finances and business regulation. The United States pushed hard for market reform in Latin America during the 1980s as a condition of debt relief. Despite resistance, efforts by Secretary of State James Baker and Treasury Secretary Nicholas Brady during the George H.W. Bush administration established neoliberal preferences for economic best practices that came to be enshrined during the 1990s as the Washington Consensus. Governments since have evaded or pushed back at such pressure. But the soft power of financial influence proves on closer inspection much softer than has often been assumed: after a certain point, as Siegel demonstrates, debtors become partners with power of their own.

Despite the potential wealth of its natural resources and growing agricultural production, tsarist Russia depended on foreign loans. A British official in 1908 likened the nation to private Russian gentlemen who despite owning immense estates lack the means of turning their possessions to account and have the utmost trouble paying their bills; he also noted a certain fecklessness in spending priorities among wealthy subjects and the state that ruled them. Developing infrastructure to exploit Russia’s potential required capital only found abroad. Rising import barriers to agricultural goods in the 1890s precluded earning the money through exports. The also contributed to weakening relations with Germany, which had been Russia’s lender and market over the previous decades.

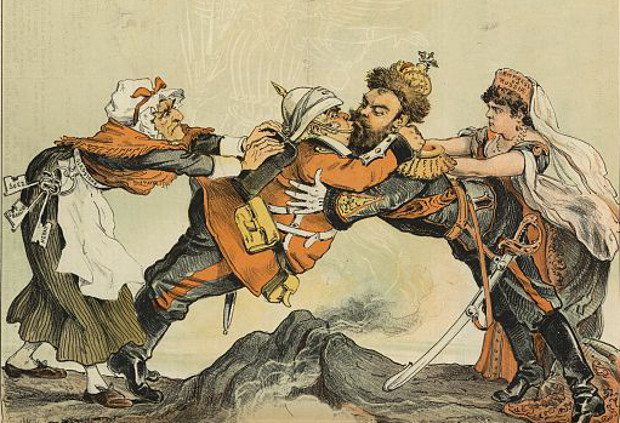

Russian rapprochement with France opened another possibility. A culture of savings across class lines gave French banks a large pool of capital that could not find adequate return from domestic investments. Small investors as a whole had more funds than the wealthy alone. The situation, as Siegel notes, made France the world’s second largest investor, with a specialty in lending to riskier parts of Europe. Russia had strong credit, having never defaulted, even during Crimean War. Its finance ministry had determined to strengthen the gold reserves backing the rouble. Good harvests combined with high prices helped restructure existing loans without further borrowing. Linking the French purse with the Russian pocket benefited both parties even before a political alliance gradually took form.

The alliance ended France’s political isolation in Europe since 1871 and gave Paris a counterweight against Germany. It also gave both parties support in their overseas rivalry with Great Britain. Shared practical interests bridged the ideological gulf between tsarist autocracy and republican France. Paris newspapers described a successful railway conversion loan in 1892 as a “financial plebiscite” in favor of the alliance. The political alliance formed in 1894 opened the way for a wave of French private lending that came to underpin Russian development projects and government finances alike.

Other political dynamics, however, complicated lending in ways that show the limited influence foreign lenders enjoyed. State-sponsored anti-Semitism in Russia appalled Jews, including the influential Rothschild banking family, which long had been loath to aid the tsarist government. The French Rothschild house changed its view and supported the 1894 loan, hoping conciliation would change Russian treatment of Jews. Other Jewish bankers, such as Jacob Schiff in New York, boycotted Russian loans. Schiff even issued half of Japan’s first war loan during the Russo-Japanese War. Yet neither engagement nor abstention had the least impact on Russian policy.

French officials and business leaders also pressed Russia to spend loans on French manufactures. Russian ministers refused to yield; as a great power, they would not be treated as a quasi-colony subject to instruction, like Turkey. Despite unease over financing purchases made elsewhere, fear of losing political support constrained France. Indeed, Russian loans had saturated the French market by 1903, forcing St. Petersburg to look elsewhere for more. The borrower had become a partner.

Russia’s financial relations with Britain took a slightly different course from the earlier alignment with France. Participation in a 1906 loan marked a thaw in Anglo-Russia relations that opened the British capital market to St. Petersburg. Financiers like Lord Revelstoke, the chairman of Barings Bank, saw it as a step toward a rapprochement between the British and Russian governments on Central Asian and imperial concerns. But only later did policy drive British investment. Many loans went to private enterprises or municipal governments as lending patterns changed after 1909. A wider range of financial institutions entered the Russian market, and the British government was much less involved with Russian loans than its French counterpart had been. Siegel points out that what seemed like the replacement of French primacy by growing British influence instead saw Russia asserting diplomatic independence. By early 1914, Russia set terms to its creditors despite being the weakest among the three powers.

The British diplomat Charles Hardinge had observed in 1901 that Russia needed peace and money to pursue the growth needed for its security. Peace involved more than avoiding foreign war. Lord Rothschild later remarked that Tsar Nicholas and his government would be safe so long as the army remained faithful, but “the safety which consists of ‘sitting on the valve’ is always the precursor of sporadic outbreaks, of dynamite outrages, of bomb throwing and assassination” and other things that “are of a nature to intimidate capitalists.” Russian officials realized their country’s precarious state. Finance minister Vladimir Kokovtsov, one of Siegel’s protagonists, consistently urged a cautious foreign policy to avoid the strain of wars.

Pyotr Nikolayevich Durnovo, Russia’s onetime interior minister, made a stronger case in early 1914 that merits attention. His plea falls outside Siegel’s story but highlights issues at stake. Indeed, Durnovo’s assessment now seems prescient. Russia lacked the industrial capacity or wealth to sustain a modern war, and the pressures of attempting to do so risked further internal unrest. Victory over Germany in World War I would have a destabilizing effect on Russia by weakening the monarchial principle, while defeat would bring catastrophe. Durnovo believed Britain meant to use Russia as a continental sword against Germany, embroiling the tsarist regime in a dispute where it had little at stake and nothing to gain. The result would shatter the peace and restrict the money on which growth relied.

The war highlighted mutual dependence. Russia relied on its allies for credit and munitions, while the French economy and the larger war effort required the Russian government’s servicing of existing debts. Britain took a hard line, insisting on the transfer of Russian gold reserves to back credit. Trust broke down even before the tsarist regime collapsed. Thereafter, a provisional government committed to maintaining relations fell to a revolution that brought to power Bolsheviks eager to make peace and unwilling to honor Russia’s debts.

Russia’s main creditors split on their response. However appalled by Communism, the British wanted reopened trade that would benefit their depressed postwar economy. The French wanted to secure investments and avoid damaging losses to their citizens. Leaders of the Soviet Union balanced their desire for global revolution with a need for capital and manufactured goods that Russia’s economy could not provide. Pressed to meet tsarist obligations, the Soviets repudiated the debt and turned to Germany, a fellow pariah in the international community. A house of cards built since the 1890s collapsed as the money need to keep it standing disappeared.

After the Soviet Union collapsed in 1991, Russia’s new government made some gestures to settle the old tsarist debt. In France and Britain the memory of bourgeois families ruined by the Bolsheviks’ default had great resonance, as Siegel notes. Even into the 1990s “la spoliation” remained a cultural reference point in France. In the 1920s, Russia’s default was seen as a case of successful repudiation that destabilized the world system and changed the assumptions of international lending. How that default came to pass highlights important facets of financial relations. Peace might have kept the system afloat despite Russia’s structural problems. Debt, as Siegel demonstrates, bolstered a tottering system and enabled Russia to operate far beyond its means. Harding’s phrase about the need for peace and money, from which the book takes its title, aptly distills the situation. Until war upset a delicate equilibrium, borrowing meant strength not weakness. Even then, lenders proved the weaker party.

William Anthony Hay is a historian at Mississippi State University.

Comments