Roadblock on Main Street

As a child in the 1950s and ’60s I lived in Red Lake Falls, Minnesota; Rushville and Muncie, Indiana; Bloomington and Springfield, Illinois; and finally Milwaukee. Their populations range from Red Lake Falls’ 1,700 to Milwaukee’s 603,000. But they had one thing in common: they all had Main Streets where people lived, worked, and shopped. Buildings typically had retail with a coffee house or barber shop on the first floor, and apartments or offices on the floor above.

But in most of America since World War II, new commercial developments have been built apart from residential spaces. Offices, too, are at a distance from everything else. As a result, Main Streets have become an historical form. They still exist, often in somewhat deteriorated condition, but almost none are newly constructed. Outside of “Main Street” at Disney’s Anaheim and Orlando theme parks, it’s hard to find a Main Street built in America since the first third of the 20th century. And it isn’t because the public demands less integrated civic space.

Americans still hold a special place in their hearts for Main Streets. “The Andy Griffith Show” and many other classic TV series were built around them. In mythical Mayberry, Floyd’s Barbershop was across from Sheriff Andy Taylor’s courthouse. Deputy Barney Fife’s fiancée, Thelma, lived in the apartment above Floyd’s. This interesting assemblage reminds me of downtown Rushville, Indiana, in 1955, when a short walk from our house at 501 Morgan Street brought my older sister and me to an ice-cream parlor owned by Mr. Gimble, whose kindly mother lived upstairs. There were coffee shops, the Durbin Hotel, and the Boys Club where I played basketball on Saturday mornings.

I visited Rushville a few years back, and the downtown is changed. The hotel is closed, and most businesses now sit in parking lots on the edge of town. This is not a natural development, a direct consequence of free-market growth and evolution. It’s in large part a result of federal housing policy.

The Federal Housing Administration was created in 1934, but it took until well after World War II for its effects to penetrate the economy. Before this, traditional streets composed of a mix of commercial and housing spaces—i.e., Main Streets—were common, partly because lenders appreciated that risk was spread over different types of real estate, which made loans safer.

For example, my uncle Earl Nelson, a D-Day veteran, became a plumber after the war. He lives in St. Paul, Minnesota, and after establishing himself in the plumbing trade he decided to start his own business. He bought a two-story building on Payne Avenue on the east side of St. Paul. It had two apartments on the second floor and space on the first floor for his plumbing company. When he applied for a loan, the banker was pleased that the building included two apartments. It reduced risk in that if the plumbing business took a while to become profitable, the apartments would provide cash flow in the meantime.

But if my uncle tried to borrow money for his building today, he would likely hear a different message from his banker. The bank would question the viability of a building that contained both a business and housing, as one or the other might fail and diminish the prospects for a return on capital and repayment of the bank’s loan. Instead of looking at the diversity of uses as a way to reduce risk, nowadays mixing of uses is considered high-risk, particularly by agencies that issue government-subsidized loans, such as the Federal National Mortgage Association (Fannie Mae).

Yet despite this regulatory stance, in recent years the desire for traditional districts has steadily gained popularity. Demographic and consumer-preference changes over the last decade have created greater demand for walkable urban real estate in communities with mixed residential and commercial uses. New development has not served this demand because federal policies and practices discourage it.

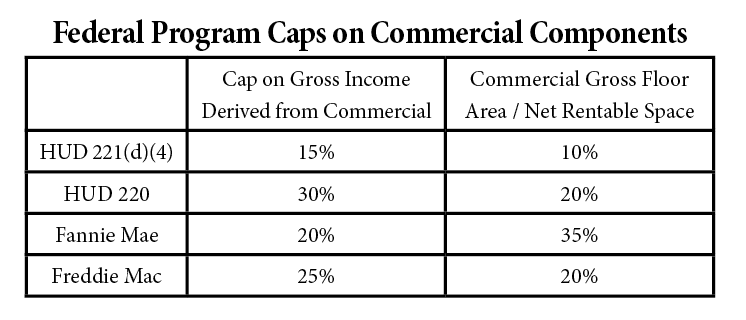

Specifically FHA, Fannie Mae, the Federal Home Loan Mortgage Corporation (Freddie Mac), and the Department of Housing and Urban Development’s 221(d)(4) and 220 programs all cap the commercial component of mixed-use real estate at a small percentage of the gross floor area/net rentable space or gross income derived from a given purpose. Combined with the tendency of private lenders to follow and apply federal underwriting rules even on loans not involving the federal programs, almost all of America’s pre-World War II Main Streets, as well as newer forms such as live/work units, are excluded from the secondary mortgage markets and HUD’s capital program for rental housing.

The percentage restrictions have no real effect on high-rise neighborhoods like the Upper East Side of Manhattan, but they have a very damaging impact on Des Moines, Grand Rapids, or even Brooklyn, where buildings have only a few floors, and thus the first-floor retail alone exceeds federal limits. Such government restrictions have dried up capital from traditional Main Streets and forcibly redirect it into developments with strictly separated uses. These regulations and regulation-inspired private lender policies obstruct the development and redevelopment of the mixed-use walkable communities that are gaining popularity with consumers.

A few years ago, I met with 17 bankers, two developers, and Chad Emerson, the economic development director for Montgomery, Alabama. I came to this meeting expecting to learn as much or more than I would impart—and I wasn’t disappointed. I described how New Urbanists such as myself looked at federal secondary-mortgage programs as unintended obstacles to urban mixed-use development. The federal programs assign extra risk to residential property associated with mixed-use buildings. I argued that these provisions undermine urban forms like Main Streets, with their low-rise apartments and condos above the stores. Then I asked what everyone thought, and after a few questions and clarifications, the bankers laid out their points of view.

One said the situation was even worse than I had described. He pointed out that it is significantly easier to sell a house if it is FHA approved. “I can sell a mortgage without FHA eligibility, but I almost feel guilty because [the buyer will] have a harder time reselling the property.” All the bankers had an interest in revitalizing downtown Montgomery, and all felt that the federal restrictions on mixed use were in need of reform.

Federal housing regulations have undeniably distorted markets and created a false standard of risk. Studies such as “The Next One Hundred Million” by University of Utah professor Arthur C. Nelson, have estimated that the current supply of unattached single-family housing already exceeds projected demand and will continue to do so until 2037. A further analysis by Nelson, “Reshaping America’s Built Environment,” indicates that even as this glut of large-lot homes continues to flood the market, the now evident demand for smaller housing in walkable traditional neighborhood settings will increase steadily and substantially.

Meanwhile, a recent Brookings Institution study—“Walk This Way: The Economic Promise of Walkable Places in Metropolitan Washington, D.C.” by Chris Leinberger and Mariela Alfonzo—highlights the economic appeal of amenity-rich, walkable, convenient communities, noting “each step up the walkability ladder adds $9 per square foot to annual office rents, $7 per square foot to retail rents, more than $300 per month to apartment rents and nearly $82 per square foot to home values.” Given the appeal evidenced by higher rents, walkable mixed-use urban development does not appear riskier than single-use developments. Arguably, programs that do not foster mixed-use should be considered riskier.

Indeed, recently Arizona State professor Gary Pivo released a report showing that the assumed riskiness of walkable urban development is misplaced. That study, “The Effect of Sustainability Features on Mortgage Default in Multifamily Housing,” finds that properties in less auto-dependent residential locations, where 30 percent or more of the workers living in the area commute to work by subway or elevated train, were 58 percent less likely to default on their mortgages.

Demand for housing types has changed markedly in recent years, and government standards should heed market demand to allow for mixed commercial-residential development, which can then act as a catalyst for economic growth and urban revitalization. Better matching of the percent limitations imposed by federal regulations on non-residential space with current demand for mixed use would spur new and diverse development, promoting further recovery of the housing market. Meeting the demand for walkable urban communities would also expand housing options for lower income people without resorting to government subsidy.

When the residential mortgage market collapsed in 2008, Democrats criticized the banking industry while Republicans blamed Fannie Mae. And of course, Democrats defended Fannie and the GOP defended the banks. Having assigned blame, Democrats and Republicans then joined together and bailed out the banks and Fannie Mae. As politicians explained the bailout to puzzled constituents, the blame-game intensified. Democrats screamed about “subprime lenders” and in 2009 passed Dodd-Frank. The GOP went after the federally sponsored and guaranteed Fannie Mae, actually calling for its abolition.

This position held until congressmen and senators visited their home districts and states and—in meetings organized by the National Home Builders Association and its local chapters—talked to contractors, developers, and realtors who saw Fannie Mae and Freddie Mac as vital sources of capital for their troubled industry. After touching base with local builder sentiment, the GOP changed its position to supporting “reform” rather than outright abolition of Fannie, Freddie, and the other federally sponsored housing programs at HUD and the FHA.

As a former big city mayor and an enthusiast for urban life, I kind of wish the Republicans had stuck to their position. And I’ve long been puzzled by the affection Democrats who represent city districts hold for federal mortgage programs, which are heavily biased in favor of separate-use zoning that is toxic for the complex, diverse, and walkable neighborhoods that are increasingly popular in American cities.

But I do credit the FHA for acknowledging, at long last, the negative effect its programs can have on Main Streets. In September of 2012, the agency relaxed the non-residential limit on the FHA secondary-mortgage program, allowing 35 percent non-residential use instead of just 25 percent. The Congress for the New Urbanism, the National Association of Home Builders, and the National Association of Realtors had encouraged FHA to recognize that the rules were obstructing consumer preference for more urban development. This small step may soon be matched with similar reforms for the vast HUD 221(d)(4) program, which is involved in financing the majority of apartments in America.

Still, when I consider the cost and perverse side effects of the FHA, Fannie, Freddie, and HUD programs, I can’t help but think that America’s towns and cities would be better off without them.

John Norquist is an adjunct professor in the Real Estate Program at DePaul University’s Business School and also serves as the John M. DeGroves Eminent Scholar at Florida Atlantic University in Boca Raton. Previously he was president of CNU and from 1988 to 2004 served as mayor of Milwaukee, Wisconsin.

This article was supported by a grant from the Richard H. Driehaus Foundation.