When The ECB Makes Monetary Policy For Germany, It’s Only Doing Its Job

I ended my post on Cyprus by talking in veiled terms about the need for institutional reform to make Europe “work.” At the risk of repeating things I’ve said many times before, let me explain what I mean.

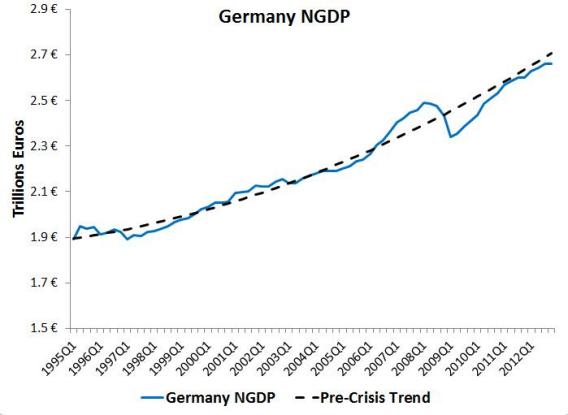

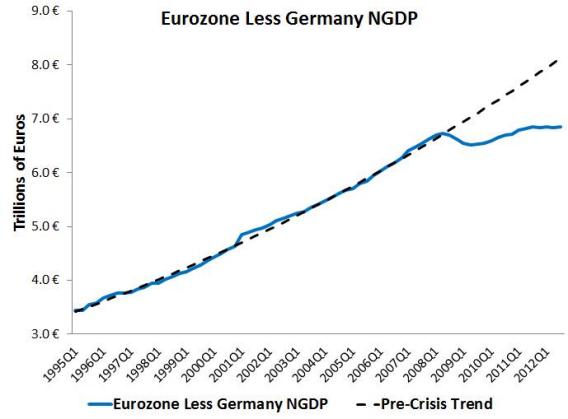

I’ll use this Matt Yglesias post as a jumping-off point. Yglesias provides two very useful graphs illustrating the success of German monetary policy (as executed by the European Central Bank), and the failure of monetary policy in much of the rest of the Euro-zone (as executed by the same monetary authority). The graphs are so good that I’m going to steal them:

As you can see, Germany’s nominal GDP has returned to the pre-crisis trend, while the rest of Europe has been limping along with virtually no nominal growth. Yglesias’s conclusion is that the ECB is basically making monetary policy with regard only for economic conditions in Germany, and without regard for policy elsewhere in Europe. And that this is both unworkable and unfair.

Unworkable it may be – but it’s exactly what the ECB was created to do. Germany’s agreement to the formation of the Euro was predicated on the assumption that the ECB would be run like the old Bundesbank. For the Euro to work, in other words, everybody would have to learn to get along with German monetary policy. A Euro that behaved like an agglomeration of the Deutschmark, the French Franc, the Italian Lira, etc. would never have been acceptable to the Germans, and everybody knew it at the time.

Not only did everybody know this, it was a major selling point for the Euro to the Southern European nations. Countries like Italy with a history of devaluation had to pay more interest on their debt than countries with more conservative monetary policy. By adopting the Euro, Italy could reduce the interest expense on its debt, precisely because the Euro would be more Deutschmark-like than Lira-like. The lower interest expense would make it less-painful for Italy to go through the structural adjustments necessary to make its economy “work” with German monetary policy, and no longer depend on periodic devaluation to maintain nominal growth. That’s why they entered into monetary union in the first place.

In effect, the Euro was never really a “currency union” but rather was a scheme by which much of Europe would adopt the Deutschmark. There are plenty of examples of countries outsourcing their monetary policy to another country with a more disciplined central bank. Ecuador currently uses the U.S. dollar as its currency, as do El Salvador and Panama and several small island nations. The Federal Reserve does not consider economic conditions in these countries when it makes monetary policy. Nor did it consider economic conditions in Argentina when it pegged its currency to the U.S. dollar in the 1990s via a currency board. No one expects the monetary authorities in Frankfurt to consider African economic conditions in setting monetary policy for the Euro, even though much of Western and Central Africa uses the CFA Franc, which is pegged to the Euro (as it was pegged to the French Franc before).

Naturally, we don’t generally talk about Italy’s participation in the Euro as being comparable to Ecuador’s adoption of the U.S. dollar, but that’s political reticence. A cold-eyed description of the transaction that created the Euro would show more similarities than differences.

Now, of course, this is all falling apart, as these things often do – the CFA Franc devalued sharply in 1994, and Argentina dropped its peg in 2002 – but it’s not falling apart because the ECB isn’t doing its job, or because Germany isn’t showing enough solidarity with Southern Europe. Such solidarity would have to be codified in political institutions, otherwise it would amount to Germany basically writing a blank check. A true fiscal union would put Germany formally on the hook for the troubles of Southern Europe – but would also give Germany more formal control over the structural adjustment process in those countries. In the absence of such, we’re seeing a series of ad-hoc negotiations between debtor and creditor nations, in which the creditor naturally holds more of the cards.

And I expect we’ll continue to do so, because the only major European nation to have expressed any enthusiasm, historically, for true political union is Germany. France in particular has always opposed any suggestion of European federalism. In big-picture terms, what Germany has been saying, pretty consistently, is: if you Southern European nations want to retain a high degree of national sovereignty, then learn to live with German monetary policy. If you want a say in German monetary policy, then you must give Germany a say in Europe-wide fiscal policy.

That sounds like a very sensible political posture to me. But I wouldn’t expect it to appeal to angry Greeks, Cypriots, Portuguese, Italians, or citizens of any other European state suffering under existing arrangements – nor would I expect the leaders of those countries to seek to enlighten them.

Comments