Everything Was Predictable In Retrospect

Paul Krugman thinks it was “obvious” that the Great Recession was going to be, well, Great, and that the various rounds of quantitative easing wouldn’t set off an inflationary spiral. I’m so glad that, in retrospect, he predicted the precise course of the financial crisis. I wasn’t so clever.

Here’s how I remember things at the time.

First, there was a real question, as late as the Lehman bankruptcy, as to whether America’s banks faced a liquidity crisis or a solvency crisis. If they faced a liquidity crisis – if all those subprime debts were ultimately good, and just distressed because the market for the debt had dried up – then the situation might have been like 1998 writ large, and emergency lending would quickly right the financial ship. The real problem wasn’t saving the economy but doing so without writing the banks a blank check. Lehman was allowed to go under precisely because the government wanted to make sure the banking sector knew that Treasury and the Fed wouldn’t be blackmailed. That bankruptcy would never have been permitted – moral hazard be damned – if the policymakers had any idea of the severity of the storm that was about the break.

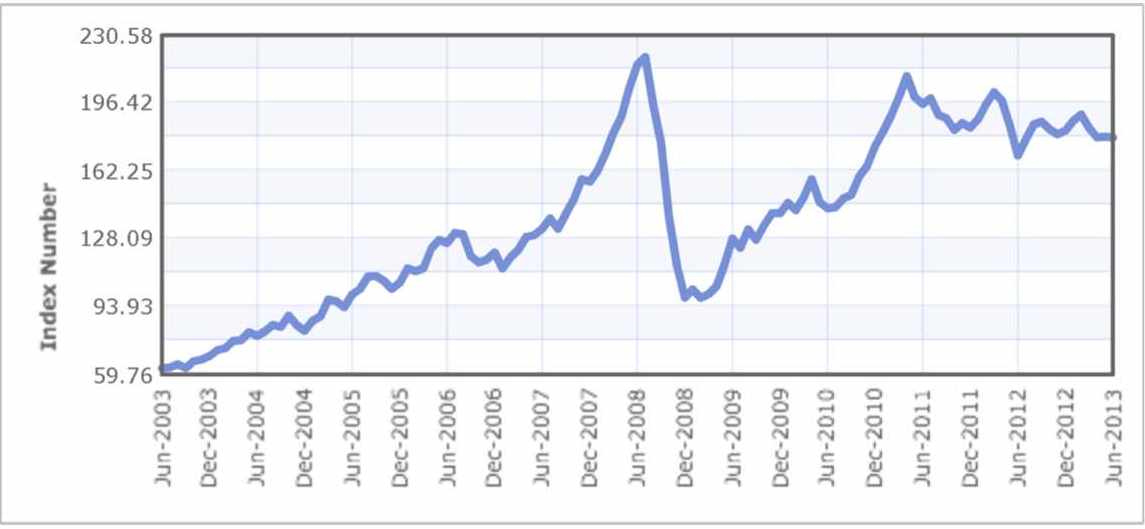

Second, in the run-up to the financial crisis, the Fed had to temper their worries about the possibility of a recession with worries about an incipient inflationary spiral. Why? Because inflation in mid-2008 was running at a 5% annual rate. China was growing like gangbusters – and its inflation rate was rising as well, and spilling over to their largest trading partners. And check out the blow-off phase of the commodities rally, which also peaked in mid-2008:

With that background, it was not completely crazy, in mid-2008, to worry that the coming recession would look more like those of the stagflation-cursed 1970s than the “postmodern” ones of the post-Cold War period (shallow and long) or the “industrial” ones of the 1950s (deep and short), and that the Fed would be stuck choosing between fighting rising unemployment and rising inflation, and end up losing both battles.

Of course, right after Lehman went bust, first the financial sector and then the real economy fell off a cliff, and both Treasury and the Fed went into crisis mode, doing whatever was necessary to stop the free-fall. But people forget how quickly it all happened, how, in the summer of 2008, lots of people – very knowledgable people – weren’t expecting anything like the level of catastrophe that then occurred. Even the smart guys who saw just how rotten things were in the sub-prime market, and put their money behind their opinions, didn’t expect the world financial system to collapse as a result. The proof it that they thought their derivatives trades with the major investment banks were solid; they weren’t worried about counterparty credit risk. Even Goldman Sachs, who were shorting their own product, didn’t think AIG, who insured that product, would go belly-up.

Both the Fed and the Treasury took extraordinary, unprecedented action in response to the financial crisis. It is not unreasonable that lots and lots of people – myself very much included – worried about the unintended consequences of that kind of action. It would be bizarre if everyone immediately and unequivocally understood that the Fed’s reaction was, if outlandish relative to baseline, quite modest relative to the scale of the crisis. It is even understandable that lots of people – some of whom write for this magazine – have felt that the failure of the Fed’s response to restore robust growth proves the validity of Austrian theories that claim, basically, that monetary policy is impossible. I think those people are badly wrong – as does almost the entire economics profession – but I understand the psychology.

I don’t see what’s accomplished by calling people who reacted this way “unreasonable” in their initial reaction. The point is: they turned out to be wrong. The issue, as Bruce Bartlett argues, is that many of them haven’t changed their tune even as the evidence has piled up on the other side of the scales.

Comments